Looking to grow your savings safely and steadily? Understanding Certificate of Deposit rates can help you make smarter decisions with your money.

Whether you’re saving for a big purchase, building an emergency fund, or just want a reliable way to earn interest, knowing where to find the best CD rates is key. You’ll discover how CD rates work, which banks and credit unions offer the highest returns right now, and tips to maximize your earnings without taking on extra risk.

Ready to make your money work harder for you? Keep reading to unlock the secrets of Certificate of Deposit rates that could boost your financial future.

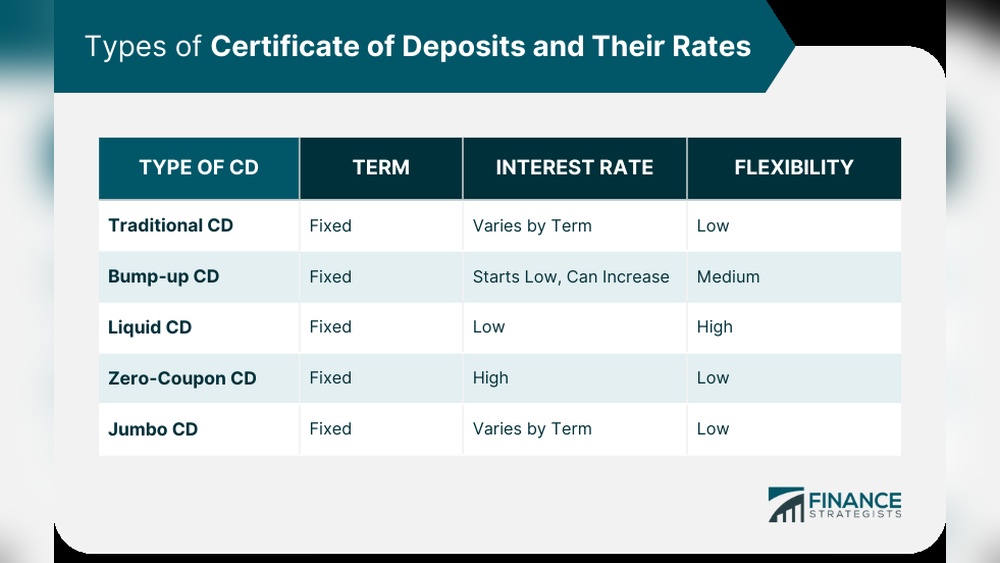

What Is A Certificate Of Deposit

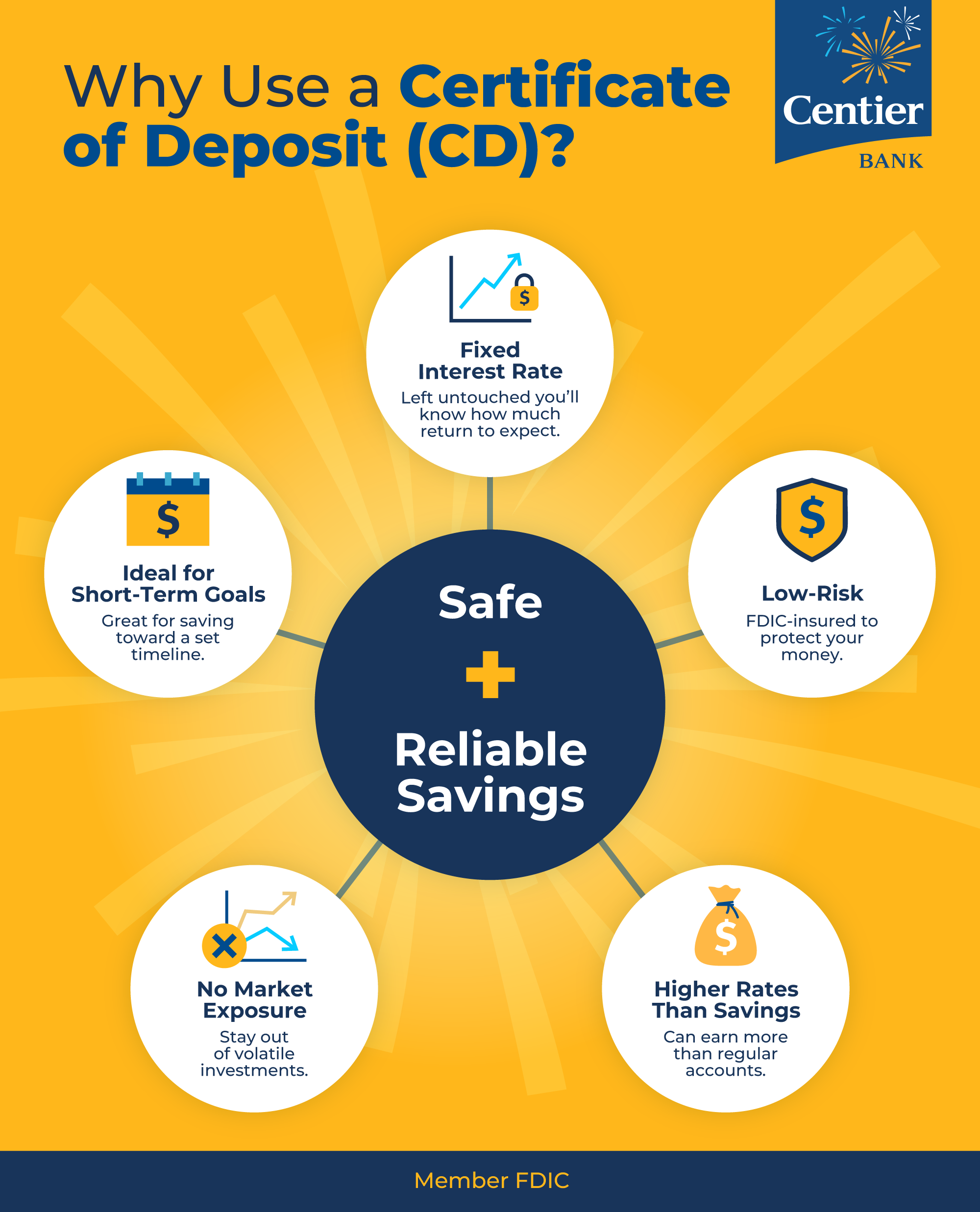

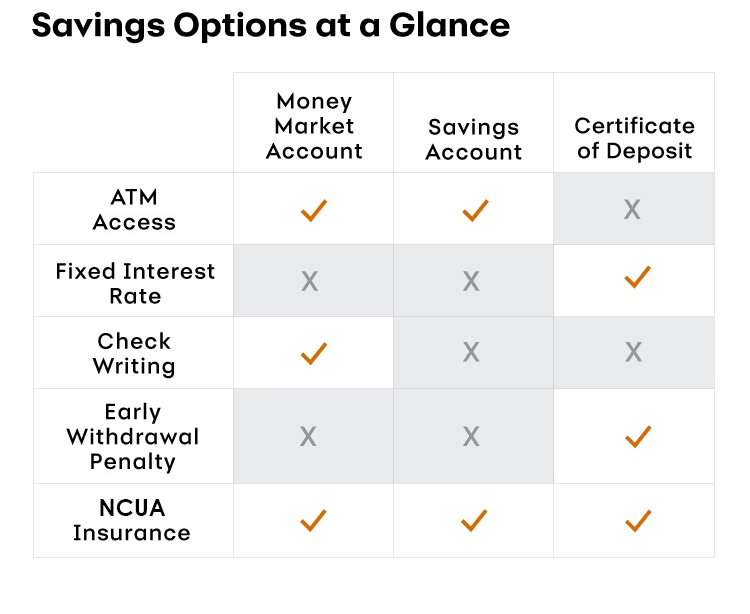

A Certificate of Deposit (CD) is a savings product from banks. You deposit money for a set time. In return, the bank pays you interest. This interest rate is usually higher than a regular savings account.

CDs have a fixed term, like 6 months or 5 years. You cannot withdraw money before the term ends without a penalty. The bank guarantees your money plus interest at the end of the term.

You choose how long to keep your money in the CD. Longer terms usually offer higher interest rates. It is a safe way to grow savings with little risk.

Current Cd Rates Snapshot

Top banks offer competitive CD rates that vary by term length. For short terms, rates are usually lower. Longer terms often have higher interest rates. Banks like Chase, Wells Fargo, and Bank of America provide a range of options.

Credit unions and online banks can offer better rates than traditional banks. They often have lower fees and more flexible terms. Online banks usually have fewer overhead costs, allowing for higher yields.

| Type of CD | Description | Pros | Cons |

|---|---|---|---|

| Brokered CDs | Sold through brokers, not banks | Higher rates, more choices | Less flexible, possible market risk |

| Traditional CDs | Purchased directly from banks | Simple, FDIC insured | Lower rates, early withdrawal penalties |

Factors Affecting Cd Rates

Term length plays a big role in determining CD rates. Longer terms usually offer higher interest rates to reward the investor for locking money away. Shorter terms tend to have lower rates but provide more flexibility.

Market and economic factors impact CD rates daily. When the economy grows, rates often rise as banks compete for deposits. During slowdowns, rates may drop as demand falls. Inflation also influences rates to keep up with rising prices.

Banks set policies based on their needs and goals. Some banks offer special promotions with higher rates to attract new customers. Others may keep rates lower to manage risk or maintain profit margins. Local competition can also affect the rates banks offer.

Choosing The Right Cd

Choosing the right Certificate of Deposit (CD) means matching the term length to your financial goals. Shorter terms offer quick access but usually lower rates. Longer terms can give higher returns but require locking money for years.

Check penalties for early withdrawal. Some banks charge large fees, while others offer more flexibility. This can affect your overall earnings if you need money early.

| Institution | APY (%) | Term Length | Early Withdrawal Penalty |

|---|---|---|---|

| Chase Bank | 3.50 | 6 months | 3 months interest |

| Wells Fargo | 3.75 | 1 year | 6 months interest |

| Ally Bank | 4.00 | 18 months | 60 days interest |

| Bank of America | 3.60 | 2 years | 6 months interest |

Maximizing Savings With Cds

Laddering strategies help spread out CD maturity dates. This means not all your money locks up at once. You buy CDs with different terms, like 1 year, 2 years, and 3 years. As each CD matures, you reinvest in a new long-term CD. This keeps cash flow steady and earns better interest rates.

Rolling over CDs means reinvesting your money in a new CD when one ends. This can keep your savings growing at good rates. Check current rates before renewing to get the best deal. Sometimes, rates go up, so rolling over can help you earn more.

Using CDs alongside other investments balances risk. CDs offer safety with fixed interest. Stocks or bonds can bring higher returns but with more risk. Mixing these can protect your money while helping it grow.

Top Banks Offering Competitive Cd Rates

Chase Bank offers a range of CD terms with reliable rates. Their CDs provide fixed interest and protection of your money.

Wells Fargo provides various CD options. They have flexible terms and competitive rates for savers.

Bank of America features CDs with different lengths. Their rates are steady and suitable for many investors.

Ally Bank is known for higher CD rates online. They offer no minimum deposit and easy access.

Vanguard and Fidelity also offer CDs, focusing on long-term savings. Their rates are good for those planning ahead.

Tools To Help Compare Cd Rates

Online rate comparison sites help find the best CD rates fast. They show rates from many banks in one place. This saves time and effort. Users can easily sort by rate, term length, or bank name. These sites often update rates daily to keep info current.

CD calculators help estimate your earnings based on different rates and terms. Enter the amount, rate, and time to see how much interest you will earn. This tool makes it simple to compare options before choosing a CD.

Monitoring rate changes is important because CD rates can change often. Setting alerts or checking trusted sites regularly helps spot good deals. Staying informed allows you to act quickly and secure higher returns.

Risks And Considerations

Early withdrawal penalties can reduce your earnings. Taking out money before the CD matures may cause a fee.

Inflation impact means your money might lose buying power. The interest earned may not keep up with rising prices.

FDIC insurance limits protect deposits up to $250,000 per bank. Amounts above this limit might not be insured.

Frequently Asked Questions

How Much Will $10,000 Make In A 6 Month Cd?

A $10,000 6-month CD typically earns between $25 and $75, depending on the current interest rate, usually 0. 5% to 1. 5% APY. Exact earnings vary by bank and rate offered.

What Bank Has The Highest Cd Rates Right Now?

Currently, banks like Ally Bank, Marcus by Goldman Sachs, and CIT Bank offer the highest CD rates. Rates vary by term and deposit amount. Check each bank’s website for the latest rates to find the best option for your savings goals.

Who Has A 9.5% Apy Cd?

Some online banks and credit unions offer CDs with around 9. 5% APY. Rates vary by institution and term length.

How Much Does A $100,000 Cd Make In A Year?

A $100,000 CD earns between $500 and $3,000 annually, depending on the interest rate. Rates vary by bank and term length.

Conclusion

Certificate of deposit rates vary across banks and terms. Choosing the right CD depends on your savings goals. Short-term CDs offer flexibility, while long-term CDs often pay higher rates. Regularly checking rates helps you find the best option. CDs provide a safe way to grow money steadily.

Keep an eye on market changes to make smart decisions. Saving with CDs can support financial stability over time. Consider your needs carefully before committing to a CD term.